The most consequential infrastructure investments today sit not within subsectors but at their intersections. Understanding them requires understanding what is shifting within each subsector first.

The definition of infrastructure is expanding, and the lines between traditional subsectors are becoming increasingly harder to draw. Power, water, transport, and digital infrastructure are becoming interdependent, both technically and economically: progress in one can be constrained by gaps in another.

Understanding those intersections requires understanding what is happening within each subsector first.

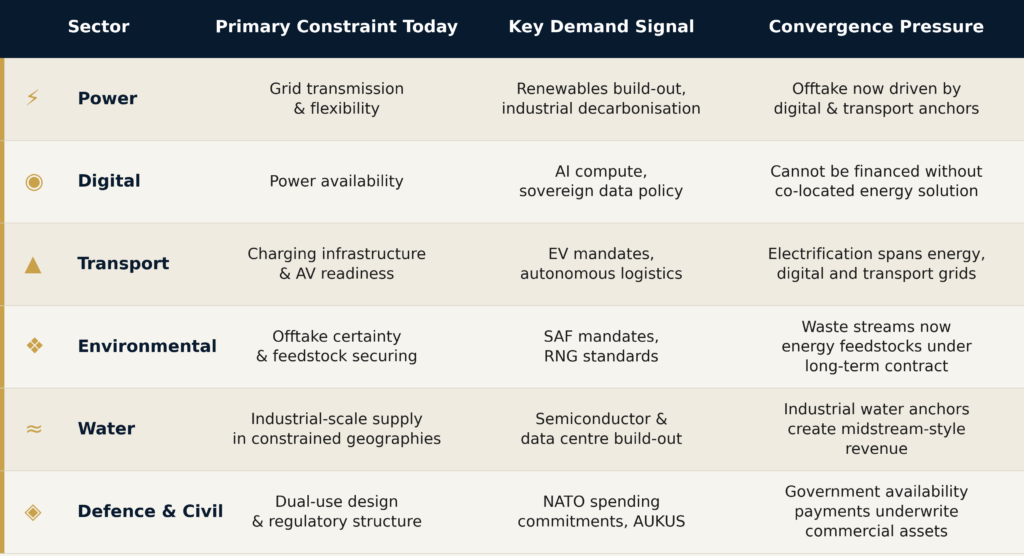

The Subsectors: What Is Changing Within Each

Power is undergoing the largest capital reallocation in its history. The IEA estimates clean energy investment reached $1.8 trillion in 2023 – exceeding fossil fuel investment for the first time. But the transition is generating structural imbalances that define today’s investment landscape. Grid infrastructure has become the critical bottleneck: in the United States, the interconnection queue has grown to over 2,600 gigawatts – more than twice the country’s total installed generation capacity. In Germany, curtailment of renewable output has cost over €4 billion in certain years because transmission and flexibility have not kept pace with generation build. The value of any energy asset is increasingly a function of its position within the broader system, not the asset itself.

Digital Infrastructure is the fastest-growing vertical by capital deployed, and it is increasingly defined not by connectivity but by power. Generative AI is the proximate cause. Hyperscale data centres consumed roughly 200 terawatt-hours globally in 2022; under accelerated AI adoption, that figure reaches 500-800 terawatt-hours by 2030. The consequence is that data centre development is no longer constrained by land, fibre, or construction capacity – it is constrained by power. Electricity consumption by data centres in Ireland reached 21% of total national consumption before authorities imposed a moratorium on new grid connections until 2028. It is no longer possible to underwrite a data centre independently of the energy infrastructure that will power it.

Transport is being restructured by electrification and automation simultaneously. Charging infrastructure is neither a transport concession nor an energy utility – it is both, and its financing, permitting, and regulatory treatment remain unresolved in most jurisdictions. Automation adds another layer: Level 4 autonomous operation requires not just a capable vehicle but a capable road environment – continuous low-latency 5G, edge computing at roadside units, and high-definition mapping infrastructure. The road is the hardware; the network is the software. Neither has full economic value without the other.

Agriculture & Waste are not traditionally considered infrastructure verticals but can now represent broader Environmental Infrastructure. Their output streams (crop residues, organic waste, carbon-rich industrial gases) are becoming critical inputs to energy infrastructure, creating contracted, long-duration revenue streams with infrastructure-like characteristics under “circular economy” initiatives. The EU agreed in 2024 to subsidise sustainable aviation fuel purchases at approximately 200 million litres annually; the US EPA’s Renewable Fuel Standard converts waste-derived gas into a premium-priced transport fuel. More than $2 billion in US private capital has flowed into anaerobic digestion infrastructure since 2020. What was an environmental liability has become a contracted cash flow.

Water is infrastructure’s most under-capitalised subsector. Global investment requirements through 2030 are estimated at $6.7 trillion; current annual investment runs at roughly $90 billion. What is changing is the emergence of industrial water demand as a distinct market. Semiconductor fabrication requires ultrapure water at extraordinary volumes – the global chip industry consumes water at a rate comparable to a city of 7.5 million people. The geographic expansion of chip manufacturing under the US CHIPS Act and equivalent EU, Japanese, and Korean programmes is placing new fabs in water-constrained locations including Arizona and Taiwan. The capital required (desalination, advanced reuse, ultrapure treatment) is structured under long-term take-or-pay agreements with creditworthy industrial anchors, a fundamentally different risk profile from a municipal water concession.

Defense & Civil Infrastructure have been converging at speed. NATO’s updated framework sets a benchmark of 5% of GDP on defence by 2035, with 1.5% explicitly designated for infrastructure – logistics facilities, airfields, naval bases, and dual-use assets. Crucially, capital is increasingly deployed through dual-use design rather than dedicated military builds: ports accommodating commercial and naval logistics simultaneously, rail corridors built to NATO axle-load specifications. The European Investment Bank has agreed to co-finance such projects under the EU’s Connecting Europe Facility, covering up to 50% of eligible costs. The blended structure reduces revenue risk while preserving commercial upside.

They key demand signals and convergence pressures are summarised below:

Nevertheless, economic sectors are no longer isolated. Capital flowing into one area increasingly shapes investment across others. As a result, McKinsey notes the rise of a broader, interconnected infrastructure ecosystem is opening significant opportunities and driving higher infrastructure investment needs than in previous decades.

The Intersections: Where the Value Lies

With those subsector dynamics in view, the convergence points become legible. These are structural collisions created by the internal shifts within each subsector described above. Notable examples include:

Power × Digital

The most capital-intensive convergence currently active is the merger of energy and digital infrastructure around AI compute power. Data centres need power; power is constrained; the two assets have become financial dependencies. BlackRock, Global Infrastructure Partners, MGX, and Microsoft’s $100 billion Global AI Infrastructure Investment Partnership pairs data centre builds with co-located renewable energy and storage as a practical necessity. Without the energy solution, the data centre is unfinanceable in constrained grid markets. Abu Dhabi’s ADQ and Energy Capital Partners have committed over $25 billion to US energy infrastructure specifically to serve data centre load.

The investment of greatest interest at this intersection is not the data centre itself, nor the renewable generation itself, but the co-located integrated platform – a single asset that generates power, consumes it for compute, and returns the economics of both to a single capital structure. The sovereign AI factory is this model at national scale: SoftBank’s 150-megawatt AI facility in Osaka targeting Japanese public-sector clients; Saudi Arabia’s HumAIn partnership to build 500 megawatts of national compute capacity under Vision 2030. In each case, the government anchor converts speculative development into infrastructure-grade investment.

Transport × Power × Digital

A charging corridor is not a transport asset, an energy asset, or a digital asset – it is all three simultaneously, requiring transport land, a grid connection, and digital management systems to function commercially. The regulatory and financing complexity this creates partly explains why Western charging deployment has lagged policy ambition. China’s deployment of thousands of fast-charging stations, with vehicle-to-grid pilots running across nine cities, has moved beyond this complexity: under V2G architecture, the EV fleet is not merely a consumer of grid capacity but a distributed balancing asset. A charging operator running V2G is no longer a transport infrastructure concessionaire – it is an energy management platform. Investors who underwrite charging networks purely as transport assets will systematically miss the value being created at that interface.

Autonomous vehicles deepen this convergence: an AV corridor requires not only charging infrastructure but also roadside edge compute, continuous 5G backhaul, and real-time HD mapping updates – layering digital infrastructure costs onto what is already a joint energy-transport asset. The capital structure for AV-ready corridors must therefore underwrite power, connectivity, and mobility as a single integrated system rather than three separate concessions, compressing the already narrow window in which mono-vertical investors can compete.

Agriculture × Waste × Power

Sustainable aviation fuel is a system investment, not a point investment. Its economics require committed feedstock supply, capital-intensive chemical conversion, distribution infrastructure, and airline offtake agreements. No single component can be financed in isolation because the returns on each depend on the development of the others. The structures that are succeeding treat SAF as an integrated capital problem rather than a single asset: Pittsburgh International Airport’s on-site production facility co-locates production with offtake, eliminating the distribution bottleneck; Australia’s Ampol-GrainCorp-IFM Investors canola-to-jet project assembles an energy company, an agricultural processor, and an infrastructure investor in a single structure. What distinguishes these from the many SAF projects that have stalled is the pre-commitment of all legs of the system before financing closes.

Digital × Water

TSMC’s Arizona fabs and Intel’s Ohio and Germany expansions require water supply solutions that do not exist at the needed scale from municipal infrastructure. The capital required is structured as long-term take-or-pay agreements with chip fab anchors, giving it the contracted cash flow characteristics of midstream energy infrastructure. The industrial water opportunity requires simultaneous fluency in water infrastructure, semiconductor manufacturing, and industrial real estate – a combination very few infrastructure platforms currently possess, which is why we believe it remains underpriced relative to its structural backing.

Defense × Civil

The dual-use infrastructure opportunity is, unusually, a government-created market with explicit policy backing. As discussed above, the EIB’s agreement to co-finance dual-use projects under the Connecting Europe Facility, covering up to 50% of eligible costs, reduces the equity requirement while preserving commercial upside. The structures of greatest interest are those where government availability payments underwrite the debt, and commercial utilisation provides equity upside. Stonepeak’s acquisitions of Forgital Group and Air Transport Services Group (neither of them traditional defense infrastructure, but both exhibiting long-term contract structures anchored by defence sector demand) illustrate how sophisticated infrastructure capital is already redefining asset eligibility to capture this dynamic.

The Investment Implication

These dynamics point to a broader shift. Infrastructure now functions as an integrated system rather than a collection of standalone assets. As interdependencies deepen, siloed approaches to planning, investment, and operations become less viable.

A transport fund that cannot underwrite EV charging because it lacks energy expertise will systematically miss the most dynamic segment of its core vertical. An energy fund that cannot value data centre offtake cannot price renewable projects anchored by hyperscaler demand.

Hence, cross-vertical platforms organised around themes rather than sectors are structurally better positioned to win the deals that matter most, because they can capture synergy value that justifies prices mono-vertical competitors cannot match while maintaining target returns.

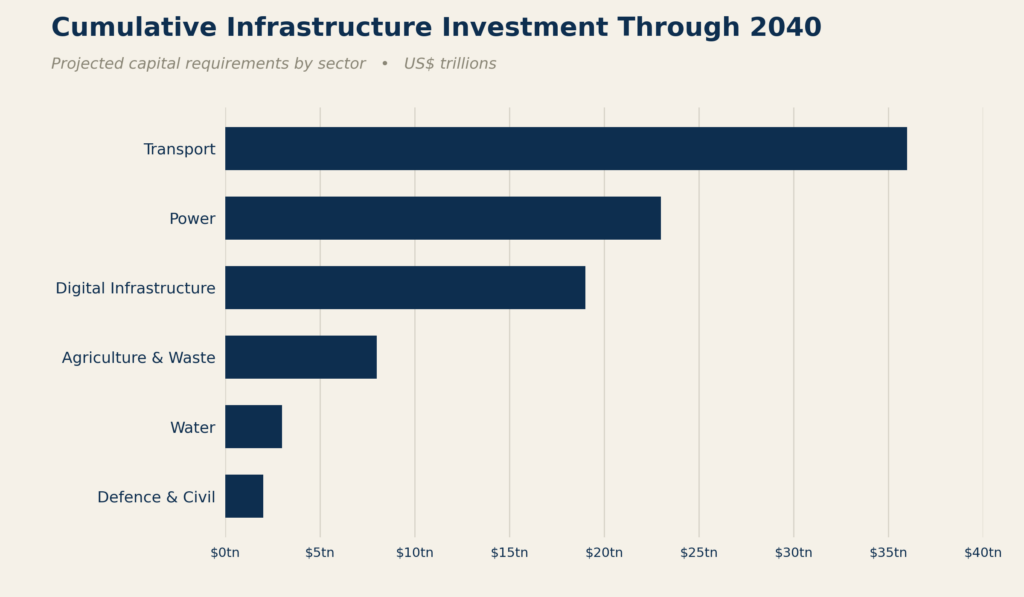

The $106 trillion in infrastructure investment required by 2040 will not flow efficiently through sector-siloed channels. Delivering the next generation of infrastructure requires cross-vertical strategies that reflect how modern infrastructure actually operates – and where value is increasingly created.

By David Dekel, Founding Associate