Over the past 20 years, the energy technology sector has experienced three distinct “hype cycles”, each characterized by initial capital surges followed by significant market corrections.

Today, the industry has entered a fourth era, defined by a broader structural imperative: sovereign resilience and self-sufficiency. Governments and institutional investors have come to recognise that the failure to secure domestic infrastructure, from power grids and gas networks to data centres and critical raw material supply chains, represents a strategic vulnerability that software-led solutions alone cannot address. What is required is technology that works with the physical asset, not around it.

This recognition is not new. Cold War-era industrial policy was built on precisely the same premise. What has changed is the urgency: modernising energy systems, securing supply chains, and building out digital infrastructure at the pace demanded by geopolitics is no longer achievable via conventional means. New infrastructure projects take decades to permit and build, where upgrades to capacity routinely lags behind the demand they are meant to serve. The result is a decisive pivot toward InfraTech: the technology required to modernise, optimise, and future-proof the world’s aging infrastructure.

The Hype Cycles

Cleantech 1.0 (2006-2011)

Driven by high oil prices and growth in generalist Silicon Valley VCs, investments on next-gen batteries & storage, thin-film solar, and biofuels sky-rocketed. For batteries, investors were looking to move beyond lithium-ion to liquid metal batteries or advanced lithium-iron-phosphate. Thin-film solar promised to make solar panels as cheap as printing newspaper. Biofuels aimed to engineer microorganisms to produce fuel that was chemically identical to crude oil.. Biofuels aimed to engineer microorganisms to produce fuel that was chemically identical to crude oil.

However, investors underestimated the capital intensity and long development cycles of hardware. The rise of cheap natural gas (fracking) and low-cost Chinese solar manufacturing led to the collapse of high-profile firms like Solyndra. Over $25 billion was invested, with more than half lost.

The Software Pivot (2012-2018)

Having suffered losses in hardware, the market pivoted to “capital-light” software, SaaS, and smart home gadgets. Investors had a goal of achieving decarbonization through behavioural change and efficiency algorithms. Instead of building a better power plant, a software can be created to convince people to use less power. Efficiency algorithms were implemented to inform a customer when to charge a battery, rather than innovating a new battery.

Unlike from 2006-2011, there were significant financial wins from this period, producing significant transactions, such as Google’s $3.2 billion acquisition of Nest in 2014 and Oracle’s $532 million acquisition of Opower in 2016. Despite this success, software alone did not reduce emissions significantly.

ClimateTech 2.0 (2019-2023)

By 2019, investors faced regulatory pressures to decarbonize. Fuelled by the Paris Agreement and “Net Zero” corporate pledges, capital was focused on electric vehicles, hydrogen, point-source capture and direct air capture, to decarbonize hard-to-abate sectors. Electric vehicle start-ups boomed with many going public via special purpose acquisition companies (“SPACs”) at multi-billion-dollar valuations before delivering a single vehicle. Hydrogen was hailed as the solution to decarbonize the energy sector, given its potential to fuel planes, ships, and steel factories. Carbon capture had the potential to allow heavy industries, such as manufacturing to continue operating as normal with more stringent emissions regulation.

In 2023, a sharp correction occurred. Interest rates rose, making climate hardware projects less attractive from an NPV perspective. Capital also grew expensive and some of the public sentiment grew tired, which stranded many pre-revenue companies requiring constant rounds of funding. Many of the electric vehicle SPACs collapsed (e.g. Lordstown Motors, Arrival) and faced large devaluations as they experienced manufacturing scaling issues. Hydrogen projects failed to reach a final investment decision (“FID”), given that there was no infrastructure in place that can effectively transport and store the gas safely. Carbon capture was technically viable but was economically difficult; later success was found when it was treated as a utility service rather than a standalone technology. Furthermore, driven by climate pledges that had failed to deliver tangible economic returns, these headwinds were compounded by a negative shift in public sentiment on ESG, which gave asset allocators further justification to scale back their commitments to climate related investments.

AI & Resilience (2025-Present)

The current era is defined by the explosive demand for power generated by the AI economy, sovereign resilience, and self-sufficiency. The explosion of generative AI has doubled data centre power demand, projected to reach 1,050 TWh globally this year. Consequently, the grid is required to expand their capacity. InfraTech solutions that specialize in Grid-Edge AI, or advanced power flow control, enable utilities to unlock latent capacity within existing infrastructure without waiting 15 years for new transmission lines.

The energy transition and AI’s expansion share a common dependency: a small number of critical minerals including lithium, cobalt, and other rare earth elements that are concentrated in a handful of countries. The IEA has stated that the demand for these critical resources could quadruple by 2040, with supply chains currently dominated by China across processing and refining. Governments across the US, UK, and Europe have responded with national critical minerals strategies and strategic stockpiling programmes. InfraTech plays a direct role in this by reducing the raw material intensity of new builds, and providing platforms that improve the visibility and management of supply chains, instruments that are now viewed as mission critical, not just as commercial tools.

InfraTech is here to stay

The ultimate lesson from the previous three cycles was that a green or AI-enabled economy cannot be achieved without the necessary infrastructure in place first. This is where InfraTech comes in to enhance existing infrastructure so that it is able to accommodate new waves of technology. According to our internal research from Preqin’s data, approximately 35% of capital deployment into infrastructure is now targeting InfraTech.

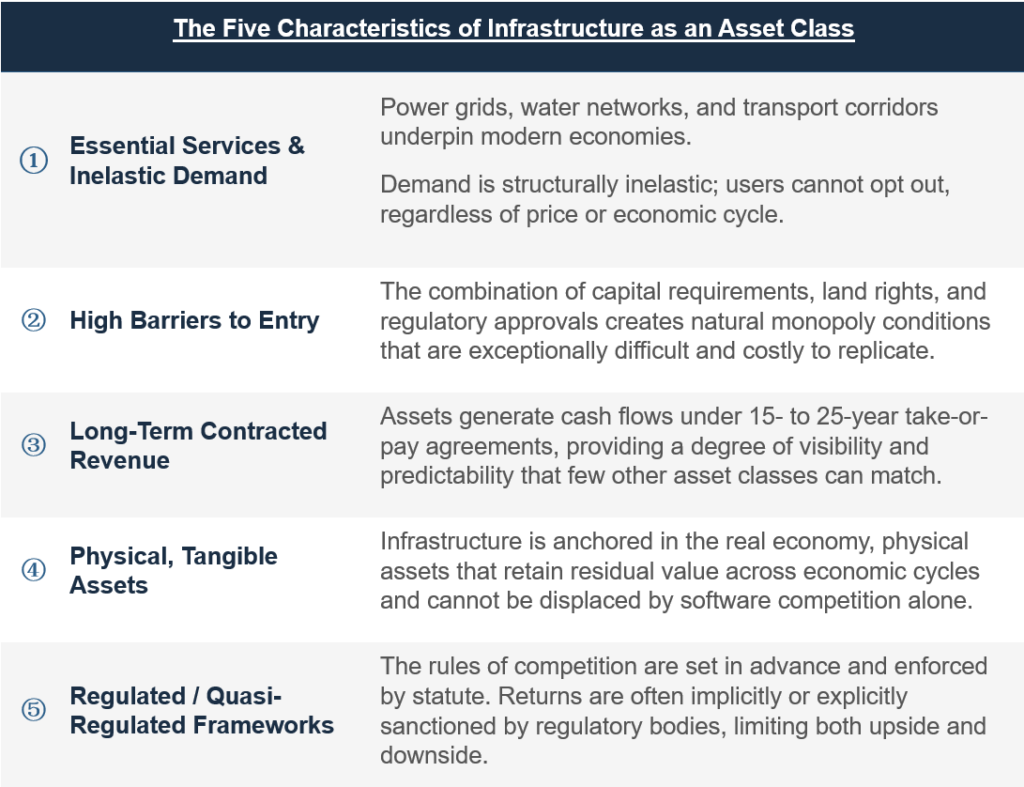

What distinguishes InfraTech from the previous hype cycles of technology is in its alignment with the five structural characteristics that define durable infrastructure assets. These are the same characteristics that have historically attracted long-duration institutional capital, explaining why InfraTech is resistant to boom-and-bust cycles:

From what is said so far, a fair question to ask would be “is this just another hype cycle like the ones before?”. Most market corrections in these previous cycles occurred because the technology fails to find a customer that is willing to pay for it. InfraTech has the opposite problem where demand exceeds supply. As long as the physical bottleneck in infrastructure exists, the technology that optimizes that bottleneck will remain a cash flow generating investment space. InfraTech is not a bet on the future, it is a necessity for today’s aging infrastructure.