The Long Road to First of a Kind

First of a Kind (FOAK) refers to the first scale deployment of a new technology. It is often associated with the valley of death, where the massive capital required to cross from pilot to commercial scale leaves many startups stranded. And just reaching FOAK does not guarantee success. Any number of missteps can leave founders, investors, and partners with little or no reward for their massive risk and efforts.

In their cleantech 1.0 postmortem[i], Bessemer Venture Partners highlight companies such as KiOR and Solyndra, each of which achieved FOAK but were extreme value destroyers. Of course, some of the world’s most successful and impactful companies also once battled to cross the valley of death: Tesla in electric vehicles, Ørsted in offshore wind, Fervo in enhanced geothermal, and General Electric in commercial nuclear power, for example.

Analysis of case studies and research from industry, academia and venture capital offers a roadmap to accomplishing FOAK successfully. It can be broken into incremental steps, sometimes iterative and sometimes parallel[ii]. While not easy, there is a path across. At which point, the valley of death becomes a competitive moat.

From Lab Table to Full Scale

FOAK is risky. The goal is to derisk as much as possible. Every question mark that can be removed increases the odds of reaching final investment decision (FID). Achieving FID requires action on multiple fronts simultaneously. Commercial and technical workstreams advance in parallel. Supplier, offtake, permitting, and land agreements progress alongside technology development, team composition, and EPC. Every milestone, such as funding stage or new deployment, triggers new and deeper iterations. And progress in one area can be the positive indicator to unlock traction elsewhere.

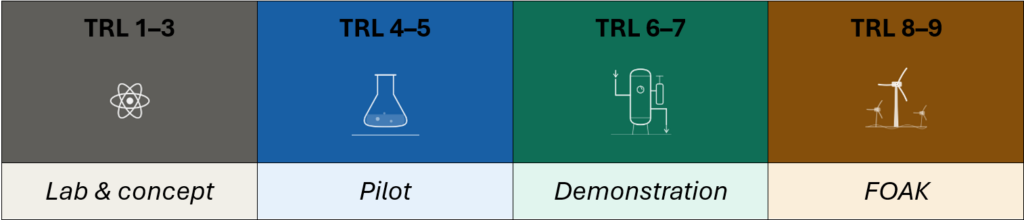

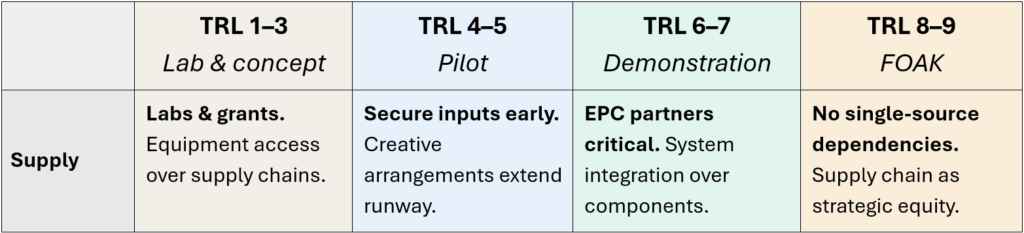

Below we examine five necessary pieces to achieving FOAK deployment: supply, demand, technology, people, and money.

Supply

Supply inputs differ between technologies. When Fervo was pioneering its first enhanced geothermal system, they partnered with operators of an existing site in Blue Mountain, Nevada. Trading upside if successful for free access to drill on the edge of the existing field[iii]. Similar approaches include asset financing of non-FOAK equipment or finding and securing decommissioned equipment to use in pilot facilities. These creative approaches secure inputs, remove question marks, and extend runway.

Startups also need engineering support. FOAK requires system coordination, as opposed to the component successes that are proven out in a lab. Programs such as Black & Veatch IgniteX and Halliburton Labs can be massive accelerators. They also offer positive signals to the market, which dovetails well with the next step: securing demand.

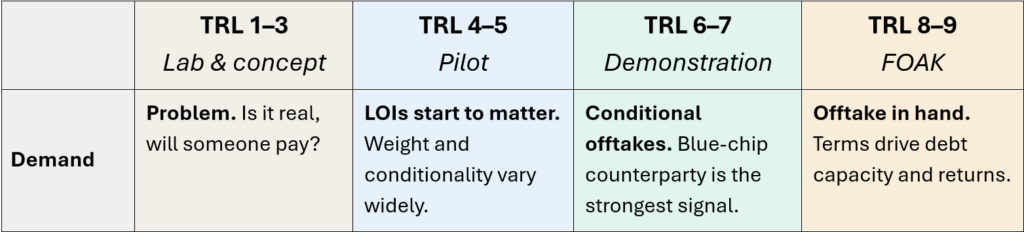

Demand

Proving demand is another key derisking lever. A common theme for early-stage investors is evaluating the weight of an LOI. They are not all built the same.

Continuing with the Fervo example, when they signed the world’s first corporate enhanced geothermal power purchase agreement with Google in 2021, it sent a powerful signal into the market, proving there was a buyer willing to pay for the output[iv].

Frontier Climate, founded by Stripe, Google, Shopify, Meta and McKinsey Sustainability fills a similar role in carbon removal. It supports carbon removal by explicitly guaranteeing carbon credit demand through a $1b market commitment[v].

Ultimately, the most powerful demand signal is a binding offtake agreement with a credible counterparty.

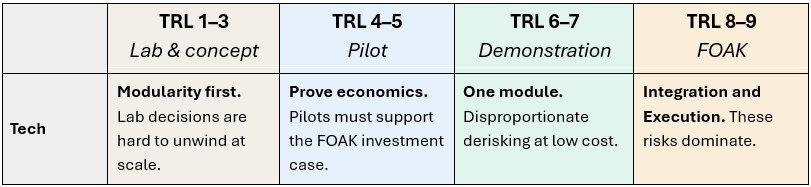

Technology

Reaching FOAK requires a startup to become a project developer. Early engineering decisions impact their ability to do so.

Modular design is one tool. Commissioning a single pilot module can have outsized impact on derisking a FOAK project. The modular approach also provides a more incremental and less steep approach to scaling. Modular allows for ongoing iteration and learning, whereas Giga-scale is binary.

Use of Commercial off-the-shelf (COTS) equipment can also derisk design and execution. Despite the name, FOAK always involves the integration of some existing technologies and processes. As explained by OCED in their comprehensive review of 21 projects, using COTS can “reduce CAPEX, simplify integration, accelerate commissioning timelines, and help get investors comfortable”[vi].

A third consideration is designing pilots to prove economics early. Pilot and demonstration plants not only prove that a technology works, they can also demonstrate a feasible path to acceptable economics at scale, unlocking a more comprehensive techno-economic analysis that supports the investment case for proceeding to FOAK[vii]. The most effective pilots are designed with this in mind from the outset.

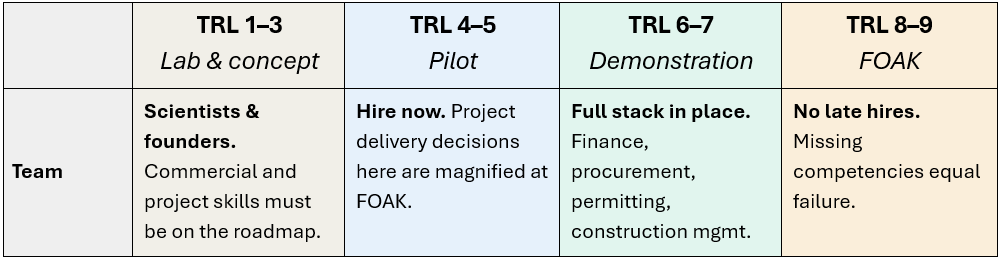

Team

Henrik Henriksson is the CEO of Stegra, a green steel manufacturing company. He founded Stegra in 2020, and during 2026 will commission a FOAK €5.5b mega-factory in Sweden. In 2023 when asked about what he could have done differently: “…maybe we waited too long to bring critical competencies into the team”.[viii]

Project delivery at large scale is a specialised trade. Finance, engineering, procurement, construction management, policy and permitting each play a role. Adding the right competencies is crucial to synthesise vision and execution. And earlier is better. Impacts of technical decisions made at pilot and demo stages are magnified at FOAK scale. The right team is not only a benefit to execution. It signals to potential partners that the company is investable. Having the right team is a core principle of venture investing. It is doubly important in FOAK given the broad range of requisite skills.

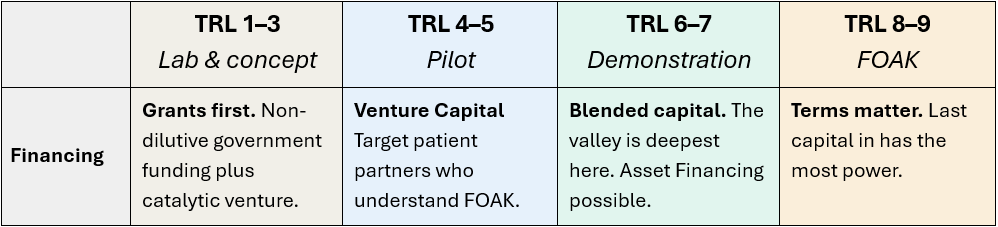

Financing

Infrastructure investments are characterised by reliable cash flows and quantifiable risk. FOAK does not guarantee reliable cash flows, requires significant investment, and the risks warrant venture, not infrastructure, returns[ix]. This leads to a structural lack of funds available to FOAK deployments. Hence the valley of death.

Strategic investors are extremely important to bridge the gap. Successful arrangements provide multi-dimensional benefits. When ArcelorMittal invested $25m into Form Energy it came with an agreement to supply iron to Form[x]. GE Vernova joined Form’s F-series while also signing a strategic collaboration MOU[xi]. Attracting investment from within the supply chain aligns incentives[xii]

Debt is harder to access than for mature technologies. Stegra used contracts (secured over years) as collateral for debt[xiii]. Equipment financing is another avenue. Grant funding rounds out the capital stack. Non-dilutive and often available specifically for FOAK-stage projects, grants can extend runway and increase investment attractiveness.

Pitfalls Along the Way

Financing FOAK is a massive lift. However, securing funds alone does not guarantee success. The terms secured are equally important. Last capital in typically has the most power, and in FOAK this is particularly true given the quantities of capital required.

Prior to bankruptcy in 2011, Solyndra undertook a massive refinancing that subordinated all previous debt and equity[xiv] [xv]. Even had the company turned around at that point, the stack of debt and preferred equity crushed the founder and early investors’ equity.

Solyndra is the extreme downside case. However, even when a FOAK company is successful there can come a time when the value of fresh capital trumps past efforts or investment. In this case, founders and early investors can face extreme dilution, or be forced to accept aggressive hurdle rates at the projectco level. Corporate structure, joint topco and projectco investments, and pre-agreed staged investments can protect founders and early investors. However, when FOAK companies slip, terms can become punitive[xvi].

Learning Curves and the Fast Follower

Another consideration – collective knowledge. While we hold Tesla up as an argument for FOAK, note that in 1996 General Motors was already producing the EV1. EV1 was a true FOAK electric vehicle, however strategic decisions led to commercial disaster[xvii]. Engineering lessons from the EV1 may have contributed to Tesla’s success as a Fast Follower.

Another FOAK success story highlighted previously was Ørsted. However, the FOAK deployment, Horns Rev 1, was not competitive with other technologies on a levelised cost of electricity basis. Learning curves, supply chains and technology improvements over multiple iterations were required before offshore wind became the UK’s cheapest source of energy[xviii] [xix].

Ultimately, leverage is gained or lost through performance, and that starts with five things: supply, demand, technology, team and money.

So, Why Take the Risk (and the dilution track)?

FOAK can unlock unfair advantages such as superior unit economics, new demand, pricing power and deep moats and defensibility. Successful FOAK also delivers returns. True North Institute looked retroactively at eight successful climatetech FOAK financing rounds from top-tier investors. They found that a single round with these companies delivered on average 2.4x MOIC and 41% IRR post-dilution[xx]. This is for companies where the average prior valuation was c. USD 300m. Very few established companies of that size return 41% IRR. Earlier stage investors expect even better returns.

Massive outcomes are possible. It requires strong partnerships, diverse and multi-disciplinary skills, and sometimes creative approaches to sourcing, building and financing. Ultimately it requires mission-driven founders, undeterred by the long road and deep valleys on the way to first of a kind.

| Michael Dirk is a Technical Partner at Actia Capital Partners and a Canadian Professional Engineer (P.Eng). He is passionate about the built world and motivated by the founders working to redefine it. |

[i] Bessemer Venture Partners, “Eight Lessons from the First Climate Tech Boom and Bust.” November 10, 2022. https://www.bvp.com/atlas/eight-lessons-from-the-first-climate-tech-boom-and-bust

[ii] Office of Clean Energy Demonstrations, FOAK Financing and Development Approaches, U.S. Department of Energy, November 2024. https://www.energy.gov/sites/default/files/2024-11/FOAK%20Financing%20and%20Development%20Approaches_112024_vf.pdf

[iii] Latitude Media, “What Fervo’s Approach Says About Financing First-of-a-Kind Energy Projects.” https://www.latitudemedia.com/news/what-fervos-approach-says-

[iv] Google, “Google and Fervo Energy Launch First-of-its-Kind Enhanced Geothermal Project,” Google Blog, November 28, 2023. https://blog.google/outreach-initiatives/sustainability/google-fervo-geothermal-energy-partnership/

[v] Frontier Climate, “An advance market commitment to accelerate carbon removal” https://frontierclimate.com/

[vi] Office of Clean Energy Demonstrations, FOAK Financing and Development Approaches, U.S. Department of Energy, November 2024. https://www.energy.gov/sites/default/files/2024-11/FOAK%20Financing%20and%20Development%20Approaches_112024_vf.pdf

[vii] Clean Energy Conversions Laboratory, University of Pennsylvania, “Techno-Economic Assessment,” CECL. https://ceclab.seas.upenn.edu/page/tea

[viii] McKinsey & Company, “Henrik Henriksson: Rapidly Scaling a Green Steel Start-Up,” November 2023. https://www.mckinsey.com/capabilities/sustainability/our-insights/henrik-henriksson-rapidly-scaling-a-green-steel-start-up

[ix] Yeh, David, and CTVC, “Venture to Project Finance Duolingo,” Sightline Climate, February 9, 2024. https://www.ctvc.co/venture-to-foak-duolingo/

[x] ArcelorMittal, “ArcelorMittal Invests $25 Million in Form Energy,” Press Release, July 22, 2021. https://corporate.arcelormittal.com/media/press-releases/arcelormittal-invests-25-million-in-form-energy

[xi] Form Energy, “Form Energy Secures $405M in Series F Financing to Expand Iron-Air Battery Business and Operations,” Press Release, October 9, 2024. https://formenergy.com/form-energy-secures-405m-in-series-f-financing-to-expand-iron-air-battery-business-and-operations/

[xii] Sightline Climate, “FOAK Financing: The Good, the Bad and the Eligible,” CTVC. https://www.ctvc.co/foak-financing-the-good-the-bad-and-the-eligible/

[xiii]McKinsey & Company, “Henrik Henriksson: Rapidly Scaling a Green Steel Start-Up,” November 2023. https://www.mckinsey.com/capabilities/sustainability/our-insights/henrik-henriksson-rapidly-scaling-a-green-steel-start-up

[xiv] Michael Scherer, TIME Swampland, “Big Name Investors Behind Obama’s Failed Green Tech Bet First in Line to Recoup Losses.” September 3, 2011. https://swampland.time.com/2011/09/03/big-name-investors-to-recoup-losses-before-taxpayers-in-obamas-failed-green-tech-bet/

[xv] Forbes, “Solyndra: Pay Some Investors Before Taxpayers In Solar Flame Out.” September 6, 2011. https://www.forbes.com/sites/toddwoody/2011/09/06/solyndra-pay-some-investors-before-taxpayers-in-solar-flame-out/

[xvi] Menoud, Laurie, “When Raising Over $1 Billion Goes Wrong: A Climate Tech Investor Cautionary Tale,” Net Zero Investor, August 27, 2025. https://www.netzeroinvestor.net/news-and-views/when-raising-over-1-billion-goes-wrong-a-climate-tech-investor-cautionary-tale

[xvii] Charles Morris, “We Should Thank the GM EV1 (And Its Death) For Tesla,” CleanTechnica, February 10, 2020. https://cleantechnica.com/2020/02/10/we-should-thank-the-gm-ev1-and-its-death-for-tesla/

[xviii] Ørsted, “Offshore Wind Energy.” https://orsted.co.uk/energy-solutions/offshore-wind

[xix] Santhakumar and Smart, “Technological Progress Observed for Fixed-Bottom Offshore Wind in the EU and UK,” Technological Forecasting and Social Change, 2022. https://www.sciencedirect.com/science/article/pii/S0040162522003808

[xx] True North Institute, “Evaluating First-of-a-Kind (FOAK) Investment Performance of 25 Leading Climate Investors,” November 2025. https://truenorthinstitute.com/resource/evaluating-first-of-a-kind-foak-investment-performance-of-25-leading-climate-investors/